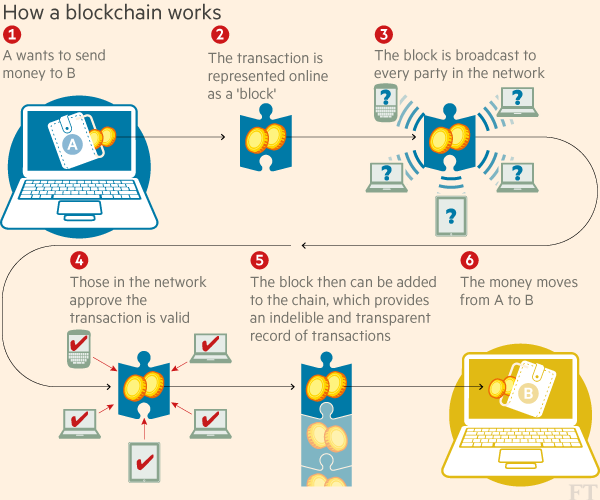

A blockchain is a ledger of records arranged in data batches called blocks that use cryptographic validation to link themselves together. Put simply, each block references and identifies the previous block by a hashing function, forming an unbroken chain, hence the name. A blockchain just sounds like a kind of database with built-in validation—which it is. However, the clever bit is that the ledger is not stored in a master location or managed by any particular body. Instead, it is said to be distributed, existing on multiple computers at the same time in such a way that anybody with an interest can maintain a copy of it. Better still, the block validation system ensures that nobody can tamper with the records. Rather, old transactions are preserved forever and new transactions are added to the ledger irreversibly. Anyone on the network can check the ledger and see the same transaction history as everyone else.

A Brief History

The first blockchain was conceptualised by Satoshi Nakamoto in 2008 and implemented the following year as a core component of the digital currency bitcoin, where it serves as the public ledger for all transactionsThrough the use of a peer-to-peer network and a distributed timestamping server, a blockchain database is managed autonomously. The invention of the blockchain for bitcoin made it the first digital currency to solve the double spending problem. The bitcoin design has been the inspiration for other applications. The blockchain format was first used for bitcoin, as a solution to the problem of making a database both secure and not requiring a trusted administrator. Today, it is considered to be a foundational technology that has the potential to create new foundations for our economic and social systems.

Why Is It Considered Revolutionary ?

-

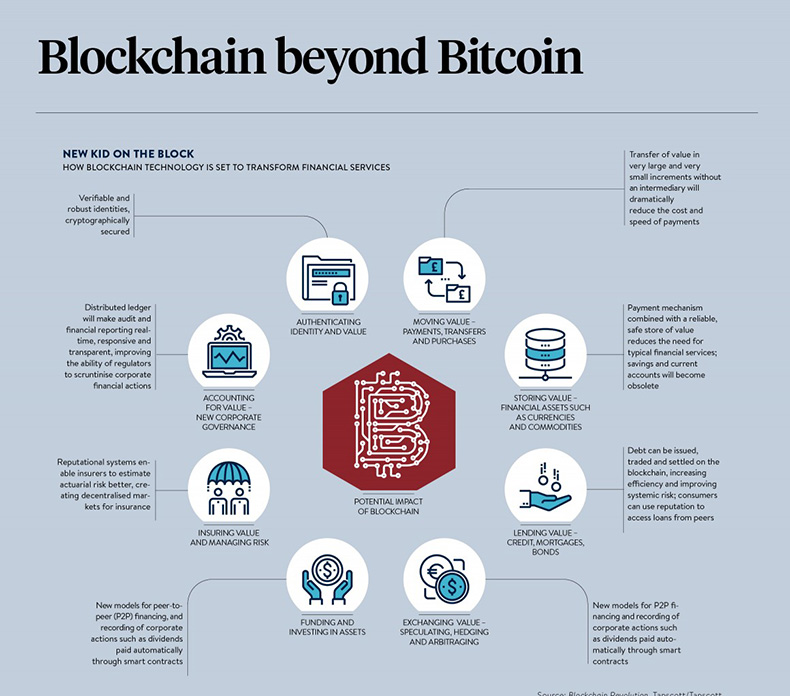

Disintermediation and trustless exchange : Two parties are able to make an exchange without the oversight or intermediation of a third party, strongly reducing or even eliminating counterparty risk.

-

Empowered users : Users are in control of all their information and transactions.

-

High quality data : Blockchain data is complete, consistent, timely, accurate, and widely available.

-

Durability, reliability, and longevity : Due to the decentralized networks, blockchain does not have a central point of failure and is better able to withstand malicious attacks.

-

Process integrity : Users can trust that transactions will be executed exactly as the protocol commands removing the need for a trusted third party.

-

Transparency and immutability : Changes to public blockchains are publicly viewable by all parties creating transparency, and all transactions are immutable, meaning they cannot be altered or deleted.

-

Ecosystem simplification : With all transactions being added to a single public ledger, it reduces the clutter and complications of multiple ledgers.

-

Faster transactions : Interbank transactions can potentially take days for clearing and final settlement, especially outside of working hours. Blockchain transactions can reduce transaction times to minutes and are processed 24/7.

-

Lower transaction costs : By eliminating third party intermediaries and overhead costs for exchanging assets, blockchains have the potential to greatly reduce transaction fees.